Brazil’s money scene is getting a massive shakeup! The Central Bank of Brazil (BCB) is throwing a curveball with a new thing called the Drex pilot. In this article, I will try to deep dive into the Drex platform, how it could totally flip the financial market on its head, and how it is putting Brazil right up there in the blockchain revolution. If you are a bit of a “gringo” when it comes to this stuff, no worries: hopefully, this will give you a clue about what is going on.

Innovation and global leadership

Brazil’s Drex pilot(a.k.a. Real Digital) is not just a digital currency initiative; it’s a paradigm shift in the financial technology landscape, setting a global benchmark for innovation. Brazil’s strategic foresight in employing blockchain technology for its national currency demonstrates a commitment to harnessing the benefits of a decentralized ledger system. This move is particularly noteworthy as it addresses the perennial issues of financial inclusivity and systemic efficiency that plague traditional banking systems.

Think of our pilot initiative as a friendly upgrade, not just a digitization of currency. We are not proposing a replacement, rather, we’re dreaming bigger! Imagine a programmable currency that can enable smart contracts, make cross-border transactions smooth as silk, and even play well with other technologies like IoT (Internet of Things). It is about transforming everyday financial activities into something more. By building a CBDC (Central Bank Digital Currency) that can give a handshake to other digital assets and old-school financial systems, we are setting up the groundwork for a comprehensive digital economy. Brazil, we are making the future happen!

Regulatory champions: BCB and CVM

The Brazilian Central Bank and the Brazilian Securities and Exchange Commission (CVM) have played a crucial role in Brazil’s fintech revolution. Their dedication to fostering a supportive regulatory framework has been instrumental in propelling the nation’s financial sector into the blockchain era with confidence.

Their strategic guidance and regulatory frameworks have not only provided clarity but also instilled confidence, empowering a spectrum of financial entities to explore the vast potential of blockchain technology. Under their watchful eye, a unique synergy has blossomed between traditional banking institutions, agile fintech companies, and innovative startups. This collaboration has cultivated a digital ecosystem characterized by robust competition and dynamic collaboration.

This harmonious digital playground has become a hotbed for innovation, where established banks are leveraging their extensive resources and customer bases, fintechs are injecting cutting-edge technology and fresh perspectives, and startups are agilely navigating niche markets. Together, they are creating a melting pot of ideas that is constantly bubbling with new, innovative solutions.

Brazil’s a big deal… maybe the biggest deal.

The BCB and CVM’s proactive approach has not only propelled Brazil to the forefront of fintech innovation but has also set a benchmark for regulatory bodies worldwide. By balancing consumer protection with innovation encouragement, they have ensured that Brazil’s financial sector remains competitive and continues to evolve with the ever-changing technological landscape. This has paved the way for initiatives like the Drex pilot, which promises to redefine financial transactions and set a new standard for digital currencies globally.

So, we have got to give a big shout out to the BCB and CVM. They’ve been total champs in pushing this innovation forward. Their rules and support have been a huge help, encouraging financial places to dive into blockchain tech. Now we have got this cool scenario where traditional banks, fintechs, and startups are all playing nice together on the same digital playground. It is all about that healthy competition and teamwork that sparks even more cool ideas.

As Brazil continues to refine Drex, it contributes valuable insights into the global dialogue on CBDCs. The country’s approach — prioritizing interoperability, security, scalability, and sustainability — provides a model for other countries to consider similar ventures.

Brazil’s economic and financial prowess undoubtedly captivates the world’s premier policymakers and financial magnates. With unwavering focus, they strive to unravel the success and challenges Brazil confronts in its trailblazing implementation of a CBDC. The knowledge distilled from this groundbreaking journey promises to offer a solid framework for other nations contemplating the inauguration of similar digital financial infrastructures. The tangible excitement surrounding these developments punctuates a critical turning point in the transformation of modern financial systems globally.

Deep diving into Drex pilot

So, the Drex pilot is an acronym for Digital, Real, Electronic, and the X conveys a sense of modernity and connection, as well as referencing Pix, the Brazilian instant payment system. It is one heck of a planned-out project. It is made to check out all the techy, operational, and strategic stuff that comes with launching a digital currency in Brazil’s mega complicated financial system. This is not just a walk in the park, it is a deep dive into all the challenges and perks that a CBDC might bring to our economy.

The pilot’s got a step-by-step approach, with each stage focusing on different parts of the CBDC’s roll-out. Each step is like abuilding block, leading us to a successful launch. We will be looking into everything — from the tech and security needed for a digital currency, to how it might shake up our monetary policy and financial stability. With this systematic approach, the Drex pilot’s hoping to lay the groundwork for a future where digital currency is a big part of Brazil’s financial scene.

Technical viability

One of the primary objectives is to evaluate the technical robustness of Drex. This includes testing its underlying blockchain protocol for throughput, resilience to cyber-attacks, and ability to handle high transaction volumes. The BCB is also assessing different technological frameworks to ensure that Drex can operate across various platforms and devices, ensuring accessibility for all users.

Operational integration

A critical aspect being tested is how Drex integrates with existing payment systems and financial infrastructures. This includes real-time gross settlement systems (RTGS), automated clearinghouses (ACH), and point-of-sale (POS) terminals. The pilot aims to ensure that Drex can be seamlessly used for both retail and wholesale transactions without disrupting current operations.

Use case exploration

The BCB is exploring a wide array of use cases for Drex, from everyday purchases to more complex financial operations like bond issuance and trade financing. The pilot is testing how Drex can facilitate micro-payments, support peer-to-peer lending platforms, and provide a stable and efficient means of exchange in digital asset markets.

Regulatory compliance

Ensuring that Drex adheres to financial regulations is paramount. The pilot is scrutinizing the digital currency’s compliance with anti-money laundering (AML) standards, know your customer (KYC) procedures, and tax laws. It also examines how privacy can be balanced with transparency to prevent illicit activities while protecting user data.

Economic impact

Beyond the technical and operational aspects, the BCB is also evaluating the potential economic implications of Drex. This includes its effect on monetary policy, implications for financial stability, and its role in fostering economic growth. The pilot considers scenarios such as inflation control, interest rate transmission, and fiscal policy coordination.

By meticulously examining these facets, the Drex pilot is setting the stage for a CBDC that is not just technologically advanced but also operationally sound and economically beneficial. It represents a holistic approach to digital currency implementation that could redefine Brazil’s monetary system and serve as a cornerstone for future financial innovations globally.

This more sophisticated analysis of the topics provides an in-depth understanding of Brazil’s pioneering work on the Drex pilot program.

Drex in phases

To give a clear understanding of the process, here is a quick summary in the seven main phases:

- Development of Drex: This phase involves conceptualizing and technically planning the Digital Real. It includes defining its scope, design, and functionalities.

- Drex Pilot: This is a testing stage for operations with Brazil’s digital currency, the Digital Real. The goal is to assess the currency’s feasibility, security, and overall functionality in a controlled environment.

- Launch of Drex: After successful testing in the pilot phase, the Digital Real will be officially launched. This marks the start of public availability, enabling secure financial transactions using digital assets and smart contracts.

- Drex and the Digital Economy: This phase emphasizes integrating Drex into Brazil’s digital economy. It highlights the currency’s role in facilitating transactions and modernizing the economy.

- Smart Products and Services on the Drex Platform: This will introduce innovative financial products and services that leverage the Digital Real platform. These include smart contracts and other digital financial instruments.

- Operation of Drex: This covers how the Digital Real functions within the Brazilian Payment System (SPB). It includes governance, regulatory compliance, and interaction with traditional banking systems.

- Drex and Digital Asset Wallet: Finally, this phase will discuss how individuals and institutions can hold and manage the Digital Real. This will be done through digital wallets designed to handle digital assets securely.

The current pilot phase is being pushed back to May 2024, so we’re still on track to launch by the end of 2024 or early 2025 according to the BCB.

The privacy component is taken very seriously, in accordance with Brazil’s General Data Protection Law (LGPD). The BCB’s team acknowledges the challenges with integration and privacy solutions. However, they want to reassure everyone that the Bank is committed to safety, and willing to spend extra time testing to ensure the platform’s technology and privacy solutions are of the highest quality.

If we want to nail this shift to a digital currency, we gotta follow a bunch of well-thought-out steps. These steps are there to make sure everything goes smoothly, and securely, and everyone involved in Brazil’s money world benefits. From the get-go with planning and development to the testing and making it happen, each step is super important for the whole thing to work out. This process ensures that not only is the digital currency tech-ready, but it also lines up with all the rules and can meet everyone’s needs. So, nailing each step is key for successfully adding digital currency into Brazil’s money world.

Drex pilot participants

Accordingo to the Brazilian Central Bank, among individual applications and consortia of entities, totaling more than 100 institutions from various financial segments, the Central Bank received 36 proposals of interest in participating in the Drex Pilot, formerly known as the Digital Real platform pilot project — RD Pilot.

In the first phase of the Drex Pilot, privacy and programmability functionalities are being tested through the implementation of a specific use case — a delivery versus payment (DvP) dApp of federal public securities between clients of different institutions, in addition to the services that make up this transaction.

This use case allows the focus of the tests on privacy since it promotes the exchange of information among the various participants of the platform, and also tests the programmability of the services offered and their interoperability.

The Executive Management Committee (CEG), based on the criteria established in the DREX Pilot Regulations, selected 16 proposals, listed below in order of registration:

- Bradesco, Núclea, and Setl

- Nubank

- Banco Inter, Microsoft, and 7Comm

- Santander, Santander Asset Management, F1RST, and Toro CTVM

- Itaú Unibanco

- Basa, TecBan, Pinbank, Dinamo, Cresol, Banco Arbi, Ntokens, Clear Sale, Foxbit, CPqD, AWS, and Parfin

- Caixa, Elo, and Microsoft

- SFCoop: Ailos, Cresol, Sicoob, Sicredi, and Unicred

- XP, Visa

- Banco BV

- Banco BTG

- Banco ABC, Hamsa, LoopiPay, and Microsoft

- Banco B3, B3, and B3 Digitas

- ABBC Consortium: Banco Brasileiro de Crédito, Banco Ribeirão Preto, Banco Original, Banco ABC Brasil, Banco BS2 and Banco Seguro, ABBC, BBChain, Microsoft and BIP

- MBPay, Cerc, Sinqia, Mastercard and Banco Genial

- Banco do Brasil

This group is a real mix! We’ve got financial institutions big and small, from S1 to S4. We’ve also got representatives from payment institutions, cooperatives, public banks, the brains behind crypto asset services, operators of financial market infrastructures, and the folks who sponsor payment arrangements.

In Brazil, the Central Bank uses segments S1 to S4 to categorize financial institutions by size and operational complexity. This helps regulate and supervise each group according to their risk profile and systemic importance. Here’s a quick rundown:

- S1: The largest financial institutions – greater than or equal to 10% of GDP with high complexity and significant impact on the financial system. Usually, these are large banks with broad national and international operations.

- S2: Medium-sized institutions – 1% to 10% of GDP – with considerable activity in the financial system, but not as large or complex as S1.

- S3: Smaller financial institutions with less complex operations – 0.1% to 1%. They are active in the market but with limited scope and scale compared to S1 and S2 entities.

- S4: The smallest institutions – inferior to 0.1% -, engaging in simpler, localized activities with the least impact on the financial system.

This segmentation is part of a regulatory framework to ensure rules applied to financial institutions match their size and complexity, maintaining a stable and efficient financial system.

Examining operational integration

The Drex pilot’s operational integration is a multifaceted endeavor, meticulously designed to ensure seamless synergy with the existing financial ecosystem. The BCB is rigorously testing the interoperability of Drex with Brazil’s renowned payment systems, such as the PIX instant payment system, and the traditional banking infrastructure. This meticulous integration process is pivotal to ensure that Drex complements rather than disrupts the current financial operations. Like mentioned before, it’s not a replacement, it’s an upgrade — Turbo mode.

The BCB’s approach involves scrutinizing the operational workflows that Drex will navigate, including retail payments, cross-border transactions, and interbank settlements. For retail payments, the focus is on ensuring that Drex can be as easily transacted as physical cash, with added benefits such as traceability and security. For cross-border transactions, Drex is being evaluated for its ability to streamline processes, reduce costs, and enhance transparency in international trade and remittances.

Furthermore, the BCB is exploring the potential of Drex in facilitating real-time gross settlement (RTGS) systems, aiming to reduce counterparty risk and settlement time in interbank transactions. This could revolutionize high-value transactions by making them nearly instantaneous and significantly more secure, as this integration of Drex with RTGS systems represents a significant area of financial innovation where specific information may be limited and highly technical.

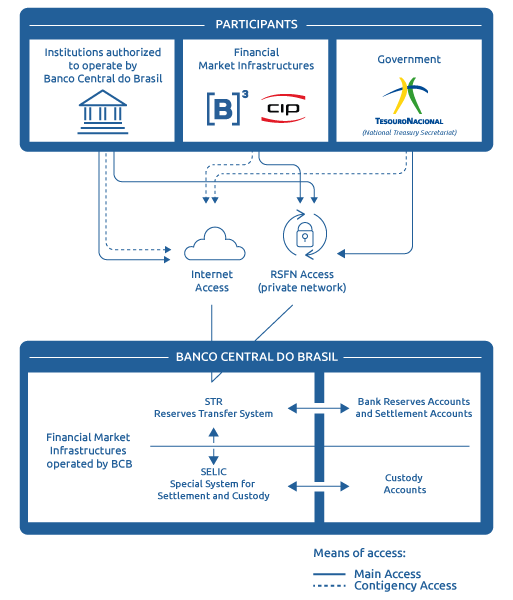

Real-Time Gross Settlement systems

RTGS systems are the backbone of high-value transactions in the banking sector, processing payments and transfers in a way that each transaction is settled individually, in real-time, and irrevocably as soon as it is processed. This contrasts with net settlement systems, where transactions are batched and settled at specific intervals throughout the day.

The main RTGS provider in Brazil is the STR (Reserves Transfer System, in English), which is managed and operated by the BCB. The STR is the real-time gross settlement system for funds transfers in Brazil, handling transactions in the monetary, foreign exchange, and capital markets among institutions that hold accounts at the BCB.Established by Circular 3100, effective March 28th, 2002, theSTRis the backbone of the Brazilian financial system, ensuring the settlement of high-value and time-critical payments efficiently and securely.

The integration of Drex, a proposed blockchain-based (DLT, but let’s use blockchain to make it easier to common understand) CBDC by the BCB, could fundamentally transform the existing RTGS infrastructure. Blockchain offers a range of advantages for transaction settlement, including increased transparency, enhanced security through data distribution, and reduction of counterparty risk because transactions on the blockchain are immutable once confirmed.

By using Drex within RTGS systems, the Central Bank of Brazil aims to achieve near-instantaneous settlement times. This immediacy is made possible because blockchain technology operates continuously, unlike traditional banking systems that may have cut-off times or require overnight processing. The reduction of settlement time from hours or days to seconds or minutes could revolutionize the efficiency of high-value money transfers.

Moreover, blockchain’s decentralized nature means that transaction records are not stored in a single location but are distributed across a network, making it significantly more challenging for cyber-attacks to compromise the integrity of financial records.

In terms of liquidity management,instantaneous settlement means that financial institutions can manage their liquidity in real-time, optimizing their cash reserves and potentially reducing costs associated with maintaining excess liquidity for transaction settlements.

The BCB’s initiative to integrate Drex with RTGS systems could set a new standard for how high-value transactions are processed both within Brazil and in cross-border scenarios. This would not only foster greater financial stability and trust in the banking system but could also place Brazil at the forefront of financial innovation globally.

For those not well-versed in Brazil’s financial system, it’s crucial to understand that it’s a mix of traditional banking operations and advanced fintech solutions. The BCB’s strategic work towards operational integration plays a key role in aligning Drex with this environment. This ensures Drex can support a wide range of financial activities without disruption.

The operational integration phase also encompasses extensive risk assessment exercises, including stress testing under various economic scenarios to ensure that Drex can withstand financial shocks and systemic stress. Additionally, the BCB is working closely with financial institutions to develop robust risk management frameworks tailored to digital currency operations.

Brazil’s financial landscape is a dynamic and complex system characterized by a mix of traditional banking operations and innovative fintech solutions.

The BCB’s strategic efforts in operational integration are vital to align DREX with this landscape, ensuring it can cater to a broad spectrum of financial activities without causing disruption.

Regulatory compliance and user privacy

The regulatory aspect of the Drex pilot is especially intricate, as it involves establishing a framework that upholds Brazil’s financial laws while fostering the growth of digital currency. The BCB is actively engaging with various stakeholders, including financial institutions, regulatory bodies, and consumer protection agencies, to ensure that Drex adheres to compliance standards such as anti-money laundering (AML) and know your customer (KYC) regulations.

User privacy stands as another fundamental pillar supporting the Drex initiative. The BCB has pledged its commitment to the design and implementation of a digital currency system that stands as a fortress, safeguarding individual privacy rights. At the same time, it recognizes the importance of maintaining an appropriate level of transparency to deter illicit activities, prevent fraud, and promote accountability.

This delicate balance is not easily achieved. It involves the development and integration of sophisticated cryptographic protocols, which are designed to anonymize transactions to a certain extent. These protocols help ensure that the identities of the parties involved are not easily accessible or decipherable, thereby enhancing user privacy.

Currently, three solutions are under consideration: Anonymous Zether from Consensys, Starlight from EY, and Parchain from Parfin, a Brazilian blockchain fintech. However, Drex participants may choose to test other solutions as well.

- Anonymous Zether from ConsenSys, is a privacy-centric payment mechanism designed for Ethereum-based blockchains. This protocol facilitates confidential transactions without needing a trusted setup. Anonymous Zether’s framework allows users to conceal both transaction amounts and the identities of the parties involved using cryptographic proofs. These proofs validate transactions without exposing the underlying information. The protocol also tackles gas linkability by suggesting transactions be dispatched from new, randomly generated Ethereum addresses with a zero gas price to maintain privacy. This feature could be particularly useful to the DREX pilot, ensuring the confidentiality of digital currency transactions on a public ledger, a key concern for central banks exploring CBDCs.

- Starlight from Ernst & Young(EY) might be related to EY’s Nightfall, an Optimistic Zero-Knowledge (ZK) Roll-Up technology initiative. This technology aims to enable private transactions on public blockchains like Ethereum. It uses ZK proofs to allow transaction verification without disclosing specific details to unrelated parties. Such technology would be critical for DREX as it would permit secure and private transactions while still leveraging the transparency and security benefits of blockchain technology. This could improve the trust and acceptance of a CBDC by ensuring user privacy and regulatory compliance.

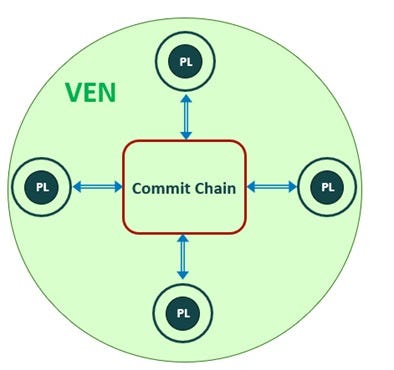

- Parfin’s Parchain is a leader in private bridges, using Zero-Knowledge and Homomorphic Encryption to outperform smart-contract based solutions. Their strategy involves establishing permissioned subnets, or Value Exchange Networks (VENs). A central blockchain, the commit chain, acts as the primary layer, with institutions using privacy ledgers as a second layer. The system’s reliability is upheld by regular encrypted commits from all privacy ledgers to the commit chain, enhanced with block hashes and Pedersen commits. Transactions between privacy ledgers remain fully encrypted, with post-quantum cryptography adding further security. Each transaction is verified by Merkle-Patricia Proofs, ensuring transaction authenticity for all VEN participants.

For each of these solutions, you can generally find further information on their respective developer platforms or by directly contacting the companies.

Integrating these technologies into Drex demonstrates the BCB’s commitment to ensuring that the digital real remains at the forefront of privacy, security, and financial technology innovation.

However, in situations where there is a legitimate need or a legal requirement, these same protocols allow for traceability of transactions. This ensures that regulatory authorities are able to access necessary information for law enforcement or compliance monitoring, thereby maintaining the integrity of the financial system while respecting the privacy rights of its users.

The challenge lies in striking an optimal balance between privacy and regulatory oversight— a task that requires innovative solutions in data protection and transaction monitoring.

The BCB’s approach includes exploring advanced technologies such as zero-knowledge proofs, which can verify transactions without revealing sensitive information.

In the context of Brazil’s financial system, which is characterized by strong regulatory standards designed to maintain market integrity and protect consumers, the introduction of Drex requires meticulous calibration. It must fit within existing legal frameworks while pushing the boundaries of what is technically possible in terms of privacy and compliance.

The complexity and sophistication of these subjects truly reflect the intricate nature and ambitious scope of the Drex pilot.

As Brazil ventures into fresh and unexplored territory with its digital currency initiative, it is setting a significant precedent for how countries around the world can harness blockchain technology in innovative ways, even within the confines of stringent regulatory environments. The wealth of knowledge and insights that will be garnered from this pilot project are not to be underestimated.

These learnings will prove to be invaluable, not only for the future of Brazil’s financial landscape but also for the global financial community as a whole. As we collectively navigate the ever-evolving and dynamic world of digital currencies, the lessons from Brazil’s pioneering Drex pilot will undoubtedly serve as a crucial reference point, guiding us towards a more digitized and inclusive financial future.

Let’s chat about digital assets rules in Brazil

The Brazilian Central Bank has been actively engaging in public consultations to refine the regulation of digital asset providers. As the deadline for submitting suggestions approached, various entities including Nuclea, Mastercard, Ripple and associations like Abcripto, Anbima, Febraban and Abranet presented their comments. Even the Digital Currency Group (DGC), which owns entities like Grayscale and Genesis, contributed suggestions.

The BCB organized the topics into several categories such as:

- Asset segregation and risk management

- Activities undertaken and virtual assets traded

- Contracting of essential services

- Governance and conduct rules

- Cybersecurity

- Provision of information and customer protection

- Transition rules; and general remarks

Here are some highlights from the contributions (by the way, Blocknewsdeserves recognition for simplifying this part of the article. If you’re interested in staying informed about Drex and the crypto economy in Brazil, it’s worth considering subscribing to their newsletter, especially if you’re not Brazilian):

But back to business…

Núclea(formerly CIP) emphasized that the control of virtual assets belongs to the holders of wallets registered on Distributed Ledger Technologies (DLTs). It stated that wallets operated by Virtual Asset Service Providers (VASPs) should be segregated to reflect that they hold customers’ cryptocurrencies. Núclea also highlighted the need for clear rules on situations where VASPs can access client wallets, such as for judicial blocking. Additionally, they suggested that regulation should include criteria similar or adapted to characterize risks associated with each DLT used for custody and transactions of virtual assets.

Febrabanstressed the importance of mitigating systemic risks to prevent the spillover of virtual asset risks into the traditional financial market. It also suggested that VASPs should not automatically gain access to market infrastructures but should meet existing eligibility requirements, but also recommending that there should be no specific regulation on the minimum percentage of assets stored in cold wallets but suggested a disclaimer informing clients about the associated risks.

These contributions form a wider BCB initiative to manage Brazil’s rapidly growing cryptocurrency market effectively, striking a balance between innovation, consumer protection, and financial stability. The public consultation process highlights the BCB’s dedication to a participatory approach in crafting policies for this evolving sector.

The FOMO phenomenon

With the Drex pilot moving forward, there’s this buzz going around in the financial world, both here in Brazil and across the globe. It’s pretty cool to see the excitement about these innovative steps we’re taking. But, we gotta be careful, right? We don’t want that ‘Fear of Missing Out’ vibe to push us into rushing things or getting our hopes too high.

The Fomoeffect, is notably strong in the fast-moving world of financial technology. Here, innovation can sometimes outpace a solid understanding of risk assessment, leading stakeholders to feel rushed into jumping on the bandwagon for fear of missing potential benefits.

It’s essential to remember that Drex, despite being a cutting-edge initiative, is currently in the pilot phase.This stage is all about exploration, experimentation, and validation, with use cases, technology frameworks, and operating models still under rigorous evaluation. Keep an eye out for those “wanna-be experts” and “Drex as a Service” solutions for stuff that’s not even fully baked or ready for the market yet.

The real benefit of Drex is its ability to enable instant and secure transaction settlement, enhancing efficiency and transparency

For those outside the pilot, robust reverse-engineering of smart contracts and insightful information are available to delve into and explore cases beyond the current pilot scope. I am confident that this proactive engagement from the “outsiders” is instrumental to the development of the ecosystem we are establishing.

Hereis one of these reverse-engineering resources — Not a recommendation, use at your own risk!

While the FOMO surrounding Drex is understandable,it’s crucial to keep a clear perspective. DREX is still in its experimental phase, with various use cases, technologies, and ideas requiring validation before transitioning into production. This validation process will ultimately determine Drex’s success and sustainability as a cornerstone of Brazil’s financial infrastructure.

Don’t get caught by the FOMO fan club

Stuff that might not go down

A very common question: is there a risk of failure or stagnation?

Yes, but it’s probably not likely. The market has already recognized the benefits of Blockchain and Asset Tokenization. There may be obstacles due to political reasons, but not because of the technology itself.

The industry must acknowledge that while Drex represents a quantum leap in conceptualizing a CBDC, the path to its full implementation is paved with complexity. Each step — from ensuring technological robustness to integrating with existing financial systems — requires “meticulous” attention to detail and an unwavering commitment to due diligence.

The BCB has clearly stated that Drex is in a development stage. It’s a space for testing new concepts, where ideas can be tested and feedback is progressively incorporated. This careful method is necessary due to the significant and extensive implications of introducing a new form of currency. It’s not only about the technology’s feasibility, but also its potential economic effects, user acceptance, and the adaptability of financial ecosystems to change.

Moreover, while Drex has the potential to revolutionize financial transactions, it is imperative to remain cognizant of the risks associated with digital currencies. These include cybersecurity threats, operational resilience challenges, regulatory compliance hurdles, and the potential for market disruption. The excitement surrounding Drex should not overshadow the need for a comprehensive risk management strategy that safeguards against these concerns.

Continuing with the pilot, stakeholders need to balance their enthusiasm with patience and caution. The development of a fully functional Drex is a long-term process, requiring a sensible approach that focuses on safety, security, and strategic planning. The industry should keep supporting the BCB in creating a strong, secure, and inclusive digital currency that aligns with Brazil’s economic objectives.

While we can’t overlook the amazing achievements of these institutions, we should also spare a thought for the challenges their employees are going through.Folks at the BCB have been dealing with salaries that don’t quite measure up to the market, sparking strikes for better career prospects and fairer wages. The situation really came to a head in September 2023 when BCB employees ramped up their protests, appealing to the government to step in and sort things out. The strikes saw a lot of workforce involvement, reminding us all of the crucial role these employees play in keeping Brazil’s financial system ticking along.

It’s pretty clear that nailing the balance between regulations and internal challenges is super important. It’s not just about cheering on innovation, it’s about making sure those amazing folks running the regulatory big shots get a fair deal. After all, they’re the ones making a huge difference to Brazil’s booming digital economy.

Just a quick “footnote” to add more context to risks (Politics)

Recently, the Brazilian government was surprised by a Proposed Constitutional Amendment (PEC) granting operational autonomy to the Central Bank, according to Brazil’s Minister of Public Service Management and Innovation. The government has not yet taken a defined position on the matter. The proposal, initiated by the opposition, will require a dialogue with the National Congress, expected to occur after the 2024 Carnival festivities (which is typically when the year truly begins in Brazil).

The Minister observed that central banks globally operate under various models. Some function as autarchies, such as the current system in Brazil, while others operate as companies. She noted that a radical change like the proposed one is quite rare.

In the upcoming days, her department will evaluate the advantages and disadvantages of converting the autarchy into a specialized company. The minister also expressed a desire to keep this discussion separate from the ongoing debate about restructuring careers at the Central Bank.

PEC 65, has been supported in the National Congress by the president of the Central Bank, Roberto Campos Neto. Last week, it was reported that the Central Bank’s Director of Administration, Rodrigo Alves Teixeira, endorsed the proposal in an email sent to employees. However, sources within the Ministry of Finance consider this discussion to be inappropriate at this time — according to the news. Politics as usual…

But how does it impacts Drex?

The operational autonomy proposal could have significant implications for the BCB’s regulatory capacity and independence, potentially affecting its role in Brazil’s fintech revolution and its ability to manage internal challenges. If passed, it could alter how the Central Bank interacts with other governmental branches and financial entities, possibly impacting its ability to support innovation while addressing employee concerns.

But let’s be optimistic.…if the BCB gains more operational autonomy, it may have greater freedom to implement and manage projects like DREX without as much direct governmental oversight. This could streamline decision-making processes and allow for more agile responses to the evolving needs of the pilot.

But quickly analyzing some of the pros and cons

Pros:

Increased Flexibility: The BCB may gain more flexibility to adapt quickly to the rapidly changing landscape of digital currencies.

Streamlined Decision-Making: Autonomy could lead to less bureaucratic interference, allowing for faster decision-making processes.

Global Alignment: The BCB could align its practices more closely with international standards, potentially leading to increased trust and investment from foreign entities.

Employee Empowerment: If autonomy leads to better career structures, it could improve employee satisfaction and retention, which is crucial for projects like DREX.

Cons:

Transition Risks: The shift to autonomy could introduce initial instability as the organization adapts to new governance structures.

Resource Uncertainty: Autonomy might lead to changes in how resources are allocated, and there’s no guarantee that projects like DREX would receive more funding or priority.

Political Challenges: Surprising the government with the proposal could lead to political pushback, potentially delaying or complicating the implementation of the DREX pilot.

The perception of the proposal as positive or negative depends on several factors, including the specific implementation of autonomy, stakeholder reactions within and outside the BCB, and the broader political and economic context in Brazil. This issue is complex and requires thorough consideration from all perspectives.

Wrapping Up

For me, this is an exciting moment. In nearly 30 years of my professional life, I’ve experienced numerous technological breakthroughs, from the BBS era, to the advent of the Internet, Mobile Internet, and multiple stages of new technologies.

The Brazilian financial landscape is on the brink of a significant transformation with the Central Bank. As said before, the Drex pilot is a major step forward for Brazil and the global financial community as it navigates the emerging realm of blockchain technology and digital currencies.

The pilot demonstrates Brazil’s dedication to innovation and inclusivity in financial services. It tackles long-standing efficiency issues within traditional banking systems while setting the stage for a future where digital and physical currencies coexist and enhance each other.

Also stands as a bold testament to Brazil’s ambition to revolutionize its financial infrastructure, harnessing the transformative power of blockchain to forge a programmable currency that can enable smart contracts, streamline cross-border transactions, and synchronize seamlessly with burgeoning technologies such as IoT. This initiative is not simply a replacement for existing financial systems, but rather a significant enhancement, offering an unprecedented level of sophistication and capability that has the potential to reshape everyday financial activities.

The BCB, CVM, Fenasbac (the Federation of the BCB Servants), and others, have been totally solid on this epic adventure. They have not merely provided regulatory guidance, but have actively fostered an environment for traditional banks, fintech companies, and startups to collaborate around a shared digital infrastructure. This thriving ecosystem is not just beneficial but crucial for sparking competition and innovation, inevitably driving the creation of robust financial solutions that are set to benefit all stakeholders.

Brazil’s been busy fine-tuning the Drex pilot, and the rest of the world’s financial big shots are all eyes and ears. The stuff we learn from this could really shake up the chat about Central Bank Digital Currencies (CBDCs). We’re talking key takeaways on making systems work together, staying secure, scaling up and keeping it sustainable. Brazil’s leading the pack here, and might just end up drafting the game plan for any other countries thinking about jumping on the digital currency bandwagon.

The Drex pilot’s operational integration is super cool, making sure that the digital real can hang out with Brazil’s famous payment systems like PIX and the usual bank stuff. The Central Bank’s careful testing of Drex’s compatibility with real-time gross settlement systems (RTGS), automated clearinghouses (ACH), and point-of-sale (POS) terminals is key to making it work. This integration is all about boosting the speed and safety of big transactions, making them almost instant and way more secure, which is great for managing cash flow and keeping things stable.

You bet, we are handling the regulatory compliance and user privacy of Drex like pros. The BCB team is totally on point, making sure Drex jives with Brazil’s financial rules and keeping user privacy safe and sound. And the best part? We’re nailing this balance using some cool cryptographic solutions like zero-knowledge proofs.

Long story short…

Brazil’s stepping up its game with this Drex pilot, trying to shake things up by going full digital on the financial front. It’s like they’re flipping the switch for a whole new phase of inclusivity, efficiency, and financial growth. This is a game-changing move that’s set to turn the traditional monetary system on its head. But it’s not just about changing things at home.

DREX is leading the charge for future worldwide financial innovations, positioning Brazil as a pioneer in digital finance.

Everybody’s holding their breath, waiting to see what happens with this giant pilot project. It’s gonna have a huge say in the future of digital currencies, not only in Brazil, but globally. This isn’t just a local shake-up, it’s gonna shift how economies across the world deal with digital currencies. From that perspective, Drex is a significant project worthy of recognition. Given time, it has the potential to significantly alter the global financial landscape by emphasizing digital currencies.